Will 3PL businesses dramatically change?

Within the scope of recent articles about imminent changes in supply chains, has been a view that the role of Third Party Logistics Services (3PL) business will dramatically change in the near future. Deliveries of goods to consumers by drone or taxi (and bicycle for congested areas) are the current examples used.

Using ‘fear, uncertainty and doubt’ (FUD) as a well entrenched method of selling a message or product; however, it does not provide an approach for executives of 3PLs to consider the future of their enterprise. Will the processes in place today be the approach used in the future?

A 3PL fits between the two parties (buyer and seller) in a commercial contract, with the role being the 3Ms – manage the movement (and storage) of materials. Based on this perception, shippers are more likely to contract out to 3PLs logistics activities that are operational, transactional and repetitive and less frequently activities which have a focus that is strategic, customer facing or core IT. Shippers are therefore likely to measure a 3PL on the basis that it provides a responsive and reliable service that is flexible to the client’s variables in demand and supply; this includes a capability to respond to major unknowns, such as natural disasters.

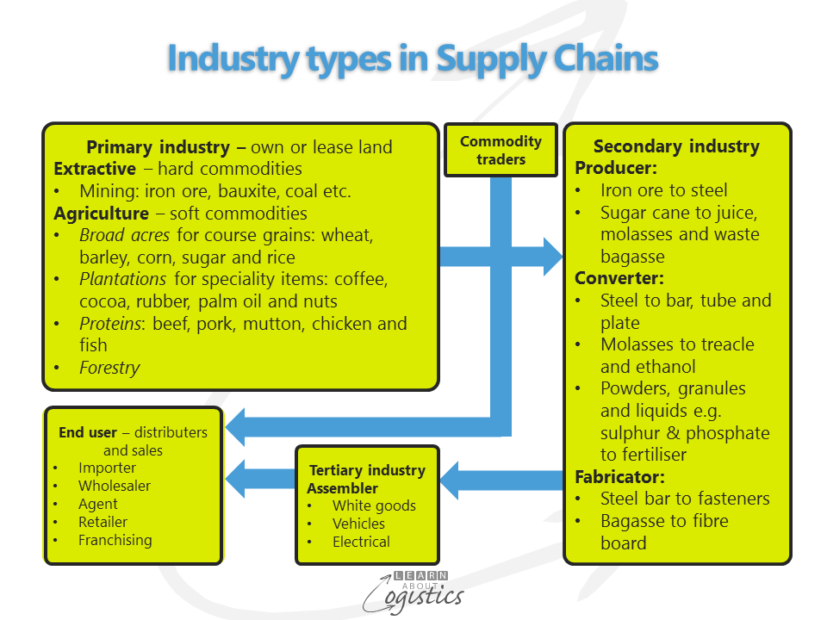

The danger with operating at the operational level is that elements of the process (or even the whole process) can be taken over by a different technology approach. The closer a business is to the ultimate consumer, the more likely this can occur. Conversely, this means the further away from consumers, the less likely will be dramatic change. The diagram identifies the flow of industry types through a supply chain, with the response of a 3PL depending on where they operate in a chain.

There are six possible 3PL relationships in consumer focused supply chains:

- Primary industry to producer: moving and storing hard and soft commodities in bulk

- Producer to converter: The output from producers is likely to be in the form of billets and ingots (discrete items) or first stage refined or processed mineral and agricultural commodities in bulk

- Converter to fabricator

- Fabricator to assembler: Fabricated items can be packaged and palletised, similar to final assembled items

- Assembler to end user (wholesalers, distributors, retailer’s distribution centres and retail sales outlets)

- Retail sales to consumer: Includes ‘courier, express parcel’ (CEP) operators

It is the last stage in a supply chain, retail sales to consumer, where change is happening and the potential for more change is most apparent; but that is not the markets where 3PLs are most established. Instead, as a supply chain becomes further away from consumers, shippers want the ‘better, faster, cheaper’ approach, but not dramatic and immediate changes in processes.

Business direction for 3PLs

For larger 3PL, the focus will most likely continue to be mergers and acquisitions (M&A), cost reduction and effectiveness, such as utilisation of assets. M&A activity could extend to combine LSPs, contract manufacturers and outsourced IT services in outsourcing markets for low end, generic, ‘complex’ but price driven products, such as automotive parts and pharmaceuticals.

Overall, the 3PL sector is fragmented, with a large number of small, owner-operator companies, most of which operate in a defined geographic region and offer limited services. Smaller companies are successful through being proficient in a service category or becoming contractors to large and mid-range 3PL companies. Three business questions for smaller 3PLs are:

- What is our business focus?

- In which product categories, industries and geographies should we operate?

- How much financial and intellectual capital should we invest?

Mid-range 3PLs have the widest flexibility to decide their business model. Time and place attributes that define Availability (the objective of Logistics) are a basis from which to define the appropriate model. The attributes are:

- Develop business relationship to better understand each client shipper’s business

- New ideas and solutions to address challenges experienced by each client shipper

- Reliability of the service provided

- Speed and response to client (the shipper) requests

- Value for money based on the service level expected (and contracted)

The scope of each attribute may be constrained by where in a supply chain the 3PL operates (the six 3PL relationships listed above), where the enterprise is located, together with the storage and ease of handling requirements for the specific materials.

At the core of the decision about which business model to adopt is the question of business identity and purpose: ‘What is the role of this 3PL business in the shipper’s supply chains?’, and ‘How can operational excellence and customer service be achieved to provide a fair return on invested capital?’